Discretionary Fiscal Policy in Japan

Source: Case Study 20.6 from MyEconsLab

You need to sign up for an account at the website to view more case studies and enrichment topics

You need to sign up for an account at the website to view more case studies and enrichment topics

1991 - 1996

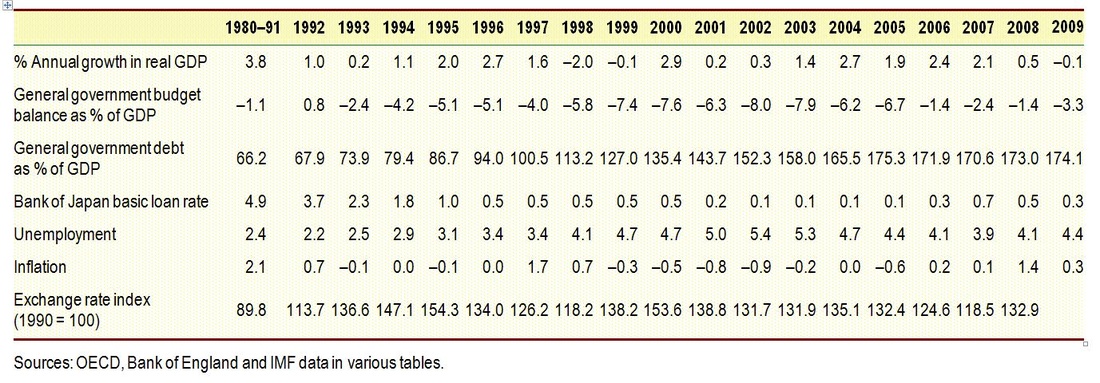

After experiencing an average annual economic growth rate of nearly 4 per cent from 1980 to 1991, it was a shock for the Japanese when the growth rate plummeted to 1 per cent in 1992, followed by a mere 0.2 per cent in 1993.

In response to the slowdown, the Japanese government injected into the economy a sequence of five public spending packages over the period 1992–6 totalling ¥59.5 trillion (£330 billion): an average increase in government spending of 7 per cent a year in real terms. There were also substantial cuts in taxes. This, combined with the economic slowdown, moved the public-sector finances massively into deficit. A general government surplus of 0.8 per cent of GDP in 1992 was transformed into a deficit of over 5 per cent of GDP by 1996 (see the table). Japan’s general government debt rose from 67.9 per cent of GDP in 1992 to 94.0 per cent by 1996.

In addition to this fiscal stimulus, the government reduced interest rates nine times, to a record low of 0.5 per cent by 1996. It also pursued a policy of business deregulation, especially within the service and financial sectors. Yet despite all these measures, it was not until 1996 that significant economic growth resumed (see the table).

Why did such an expansionary fiscal (and monetary) policy prove to be so ineffective? The answer can be found in the behaviour of the other components of aggregate demand.

In previous decades, the prosperity of Japanese business was built upon an export-led growth strategy. If there was a lack of demand at home, surplus capacity in the economy could simply be exported. But this option was no longer so easy. Since 1985 there had been a massive appreciation of the exchange rate: the yen rose by over 150 per cent against the US dollar in the ten years up to 1995. This, plus growing competition from other Asian exporters, meant that Japanese firms were finding it harder to export.

In response to the slowdown, the Japanese government injected into the economy a sequence of five public spending packages over the period 1992–6 totalling ¥59.5 trillion (£330 billion): an average increase in government spending of 7 per cent a year in real terms. There were also substantial cuts in taxes. This, combined with the economic slowdown, moved the public-sector finances massively into deficit. A general government surplus of 0.8 per cent of GDP in 1992 was transformed into a deficit of over 5 per cent of GDP by 1996 (see the table). Japan’s general government debt rose from 67.9 per cent of GDP in 1992 to 94.0 per cent by 1996.

In addition to this fiscal stimulus, the government reduced interest rates nine times, to a record low of 0.5 per cent by 1996. It also pursued a policy of business deregulation, especially within the service and financial sectors. Yet despite all these measures, it was not until 1996 that significant economic growth resumed (see the table).

Why did such an expansionary fiscal (and monetary) policy prove to be so ineffective? The answer can be found in the behaviour of the other components of aggregate demand.

In previous decades, the prosperity of Japanese business was built upon an export-led growth strategy. If there was a lack of demand at home, surplus capacity in the economy could simply be exported. But this option was no longer so easy. Since 1985 there had been a massive appreciation of the exchange rate: the yen rose by over 150 per cent against the US dollar in the ten years up to 1995. This, plus growing competition from other Asian exporters, meant that Japanese firms were finding it harder to export.

Japanese Macroeconomic Indicators 1980 - 2009

As far as investment was concerned, the slowdown in the economy and sluggish export sales, plus high levels of debt from the expansion of the late 1980s, reduced profits to near record lows and created a climate of business pessimism. After increases in investment averaging 10 per cent per year from 1987 to 1990, investment fell for three successive years after 1991.

Consumers too were in a pessimistic mood. Even with a ¥5 trillion cut in taxation in 1994, consumer spending on domestic goods and services grew only marginally, whereas saving increased sharply, as did imports.

Even though the total fiscal stimulus over the period was large, the incremental nature of the government’s action failed on each occasion to stimulate business and consumer activity to any significant degree.

Consumers too were in a pessimistic mood. Even with a ¥5 trillion cut in taxation in 1994, consumer spending on domestic goods and services grew only marginally, whereas saving increased sharply, as did imports.

Even though the total fiscal stimulus over the period was large, the incremental nature of the government’s action failed on each occasion to stimulate business and consumer activity to any significant degree.

1997 - 2002

The recovery of 1996 was short lived. With other countries, such as Thailand and Indonesia, experiencing a large economic downturn in 1997, and with a growing mood of pessimism across the region, the Japanese economy plunged into recession. By 1998, amidst bank failures and speculative outflows of money from the country, the Japanese economy was in a state of crisis. The government’s response was once more to resort to fiscal policy.

A ¥16 trillion (£80 billion) expansionary fiscal package in April 1998, was followed six months later by another package worth over ¥18 trillion (£90 billion). This second package included over ¥10 trillion on public works projects and cuts in the maximum rate of income tax from 65 per cent to 50 per cent (worth ¥4.2 trillion) and substantial cuts in corporate taxes. One novel feature of the package was the distribution of shopping vouchers to 35 million citizens: the elderly and families with young children. These free vouchers were worth ¥700 billion (£3.5 billion).

One of the biggest problems in stimulating the economy was the very high marginal propensity to save. Given the continuing pessimism of workers about the security of their jobs, many people responded to tax cuts by saving more, especially given that prices were stable or falling and hence the value of money saved would not be eroded by inflation. Even the shopping voucher scheme had limited success, as people used them to replace existing expenditure and saved the money that they no longer needed to use.

Another problem was the mood of businesses. With banks collapsing under the weight of bad debt, with loans to industry consequently cut, with Japanese companies eager to cut costs, and with business pessimism about consumer and export demand, investment was being cut back. Reductions in business taxes were not enough to reverse this.

A modest recovery was under way in 2000 (see the table), but in 2001, with the USA slipping into recession and with the European economy slowing down, Japanese exports began to fall and a mood of pessimism rapidly returned. The government had hoped that supply-side reforms to make the economy more competitive would work, but these are long-term policies and the problem was immediate.

So what could be done? The answer was very little. With interest rates of virtually zero, there was little scope for an expansionary monetary policy, and with a general government deficit of over 6 per cent and a national debt of over 140 per cent of GDP and rising, there was now little scope for fiscal policy either. All that could be done was to wait for the recovery in the world economy and for the supply-side reforms to begin to work to make Japanese industry more competitive.

A ¥16 trillion (£80 billion) expansionary fiscal package in April 1998, was followed six months later by another package worth over ¥18 trillion (£90 billion). This second package included over ¥10 trillion on public works projects and cuts in the maximum rate of income tax from 65 per cent to 50 per cent (worth ¥4.2 trillion) and substantial cuts in corporate taxes. One novel feature of the package was the distribution of shopping vouchers to 35 million citizens: the elderly and families with young children. These free vouchers were worth ¥700 billion (£3.5 billion).

One of the biggest problems in stimulating the economy was the very high marginal propensity to save. Given the continuing pessimism of workers about the security of their jobs, many people responded to tax cuts by saving more, especially given that prices were stable or falling and hence the value of money saved would not be eroded by inflation. Even the shopping voucher scheme had limited success, as people used them to replace existing expenditure and saved the money that they no longer needed to use.

Another problem was the mood of businesses. With banks collapsing under the weight of bad debt, with loans to industry consequently cut, with Japanese companies eager to cut costs, and with business pessimism about consumer and export demand, investment was being cut back. Reductions in business taxes were not enough to reverse this.

A modest recovery was under way in 2000 (see the table), but in 2001, with the USA slipping into recession and with the European economy slowing down, Japanese exports began to fall and a mood of pessimism rapidly returned. The government had hoped that supply-side reforms to make the economy more competitive would work, but these are long-term policies and the problem was immediate.

So what could be done? The answer was very little. With interest rates of virtually zero, there was little scope for an expansionary monetary policy, and with a general government deficit of over 6 per cent and a national debt of over 140 per cent of GDP and rising, there was now little scope for fiscal policy either. All that could be done was to wait for the recovery in the world economy and for the supply-side reforms to begin to work to make Japanese industry more competitive.

2003 - 2007

By 2003, the Japanese economy at last seemed to be recovering and for the next four years it managed to achieve moderate economic growth. But consumer spending remained hesitant and a persistently high value of the yen curbed a growth in exports.

As the recovery continued, the government attempted to rein in government spending and the general government deficit fell (see table).

From 2006, inflation at last turned positive. The hope was that this would discourage people from saving cash and that this could give a boost to consumer demand.

As the recovery continued, the government attempted to rein in government spending and the general government deficit fell (see table).

From 2006, inflation at last turned positive. The hope was that this would discourage people from saving cash and that this could give a boost to consumer demand.

2008

But the recovery was fragile and with the world economy slowing rapidly in 2008, so too did the Japanese economy. Japan once more resorted to expansionary fiscal policy (and monetary policy too). In August 2008 parliament passed an ¥11.7 trillion (£56.8 billion) stimulus package. Then in October 2008, the government announced that it was considering a further ¥27 trillion (£170 billion) of extra government spending and tax cuts.

By early 2009, GDP was falling fast – at an annual rate of 12.7 per cent. Parliament passed the government’s stimulus plan, which had been firmed up since it was proposed the previous October. This included most people being given ¥12,000 (£90) as a cash hand-out. But, as before, the question was whether people would spend the money or merely save it, fearing that times would get tougher.

By early 2009, GDP was falling fast – at an annual rate of 12.7 per cent. Parliament passed the government’s stimulus plan, which had been firmed up since it was proposed the previous October. This included most people being given ¥12,000 (£90) as a cash hand-out. But, as before, the question was whether people would spend the money or merely save it, fearing that times would get tougher.